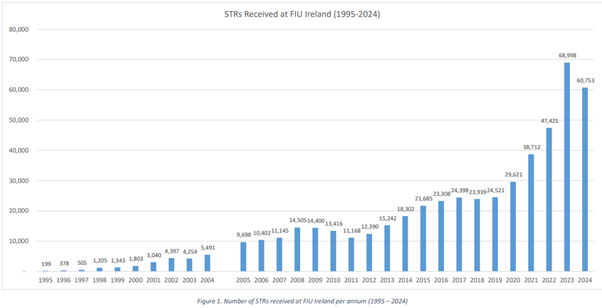

STRs Received at FIU Ireland (1995-2024)

1. Summary i. STR Volumes:

ii. Main Reporting Entities (2024):

iii. STReu (European Union reporting obligation):

2. What’s interesting i. VASPs volatility in STR reporting:

ii. E-Money Institutions as major STR drivers:

iii. Persistent dominance of banks but diversification of sources:

iv. International cooperation obligations:

0 Comments

More than €90,000 seized in money laundering investigation [September 14, 2025]

1. Summary: i. Over €90,000 in cash was seized in a money laundering investigation in Ireland, focused on large cash withdrawals from ATMs in Dublin and Cork. The Garda National Economic Crime Bureau (GNECB) led the operation, which followed transactions between 11 August and 9 September 2025. ii. The withdrawals used bank cards linked to accounts based in Poland and Norway. During the operation, a vehicle was searched in Lucan, Dublin on 13 September, where a substantial amount of cash and multiple bank cards were recovered. A male in his early-30s was arrested under relevant sections of Irish law. iii. Later, a woman in her 30s was also arrested at a Dublin address. Additional searches in Cork recovered more cash, foreign currency, false ID documents, bank cards and mobile phones. Gardaí are cooperating with international law enforcement through Europol in relation to the foreign bank accounts connected to this case. Both suspects remain in custody and the investigation continues. 2. What’s interesting i. Cross-border bank accounts & multi-jurisdictional risk

ii. Large cash withdrawals from ATMs as a red flag

iii. Use of multiple bank cards and false IDs

iv. Timing / detection window

v. Asset seizure & law enforcement cooperation

vi. Use of false/fraudulent documentation / identity fraud

vii. Potential reputational & regulatory risk

Source: https://www.breakingnews.ie/ireland/more-than-90000-euro-seized-in-money-laundering-investigation-1806873.html  Student charged with money laundering after agreeing to act as money mule for text scam [September 12, 2025]

Summary: i. A 20-year-old student, Darragh Sutcliffe, pleaded guilty to money laundering after agreeing to act as a money mule for a “smishing” (text phishing) scam. He had no prior convictions. At the time of the offence, he was planning to sit accountancy exams. ii. Between 23-25 May 2023, €16,350 in fraudulently obtained funds from smishing scams were deposited into his account in four separate transactions. €9,350 came from one victim (Cork woman) via an “E-flow text scam” after she responded to a malicious message. Another €2,000 from a Killarney resident. iii. Sutcliffe withdrew about €3,500 from ATMs in Lucan before his bank froze his account. After his account was flagged, he went to Gardaí and made a false report to try to distance himself from the transactions. The banks reimbursed the victims, except AIB remained out €3,500 (the ATM withdrawals). iv. In court, his solicitor emphasised that he was a typical “non-complicit money mule” — i.e. someone who allows just their account to be used on promise of payments which never materialised. v. He’ll repay the stolen funds, was contrite, has family support; sentencing has been adjourned until February. The judge also ordered a €5,000 donation to a cancer charity. 2. What’s interesting: i. Money mule risk & identification

iii. Bank account usage, transaction monitoring, freezing mechanisms

iv. False reports / attempts to distance oneself

v. Financial harm & liability:

vi. Education & awareness as mitigation

vii. Sentencing & regulatory implications

Source: https://www.irishexaminer.com/news/arid-41704397.html  Four charged in connection with international money laundering probe [September 8, 2025]

1. Summary i. Four people in central Dublin have been charged with money laundering involving proceeds of crime, in amounts ranging from around €29,000 upwards. ii. The investigation is being carried out by An Garda Síochána’s GNECB (Garda National Economic Crime Bureau) under organised crime legislation. iii. The alleged laundering involved use of bank accounts in Poland and Norway; there were large cash withdrawals from ATMs in Dublin and Cork over a period (11 August - 9 September 2025). iv. Items seized include cash, bank cards, false identification documents, and mobile phones.

ii. ATM cash withdrawal patterns as red flags: Repeated, large withdrawals via ATMs in different locations (Dublin & Cork), often a sign of layering or attempt to extract physical cash; good reminder to ensure outbound cash flow monitoring is strong (not just deposits). iii. False identities & multiple devices: Use of false IDs, multiple bank cards, mobile phones suggests efforts to obscure identity, complicate tracing. Reinforces the importance of strong identity verification (KYC), device monitoring if relevant, and forensic recordkeeping. iv. Regulatory / legal tools in play: Use of organised crime and criminal justice legislation (Sections under Irish law) shows that law enforcement is using serious legal powers. For compliance programs, this implies that suspicious activity reports (SARs) etc. must be airtight; any lapses could lead to legal/regulatory exposure.

Very good AML typology on money mules and goes to show that highly educated people can be sucked-in to money laundering. I posted about it on Linkedin here and a guest contributor also wrote a detailed piece here. Noting this person's background of a business degree and work at an airline and tech company, quite possible that a career in financial services may be on the cards. That is certainly not over, but there will be a big hurdle to clear because the fact that no conviction was recorded doesn't mean that the person does not have to disclose it, It will raise concerns about judgement with a potential future regulated financial services provider employer. ➡️ A business graduate who let her “con-artist boyfriend” use her bank account to launder money has been spared a criminal record. ➡️ Chelsea Stelma Cassule (25) had been taken into her then partner’s trust when she gave him access to her account, which was used to transfer the €300 proceeds of a fraud. ➡️ Judge John Hughes struck the case out at Dublin District Court after hearing she had made a €300 charity donation and a probation report put her at a “low risk” of reoffending. ➡️ Cassule, of Brabazon Hall, Cork Street, Dublin 8, had pleaded guilty to money laundering – possession of the proceeds of criminal conduct. ➡️ Cassule had no previous convictions. ➡️ A defence barrister said the third party was Cassule’s boyfriend at the time. He told her he had a job opportunity in Belfast and was going to move there but needed a deposit and asked to use her account. ➡️ She did not know her boyfriend was defrauding anyone but in the cold light of day, she accepted the story was “a little bit fanciful”, the barrister said. ➡️ The accused had a business degree and had worked for an airline and a tech company. ➡️ Judge Hughes said Cassule had been “a victim of this herself” and had not made any financial gain. Her “con-artist boyfriend” had “taken her into his trust” and her suspicions were lowered, but she “should have known better”, the judge said. ➡️ The accused had an otherwise “unblemished” record. Source: https://www.independent.ie/irish-news/courts/woman-who-let-boyfriend-use-her-account-for-money-laundering-avoids-criminal-record/a1373019726.html

Woman who let boyfriend use her account for money laundering avoids criminal record [September 3, 2025]

1. Summary: i. A business graduate allowed her “con-artist boyfriend” to use her bank account for money laundering. ii. She was spared a criminal record in relation to that offence. iii. Her defence emphasised that she had been manipulated / misled by her partner, and that her involvement was passive (i.e. letting use of account rather than actively operating the laundering) and that she did not profit. iv. The court considered her personal circumstances (e.g. being misled, her lack of awareness of full criminality) when deciding to not impose a criminal record. 2. What’s interesting: i. Non-complicity / Naivety” defence

ii. Risk of insiders or account holders being exploited

iii. Court leniency & thresholds for criminal record

iv. Implications for account monitoring / KYC / due diligence

|

AuthorOn this page you will find a selection of links to articles useful for AFC training. Archives

September 2025

Categories

All

|

RSS Feed

RSS Feed