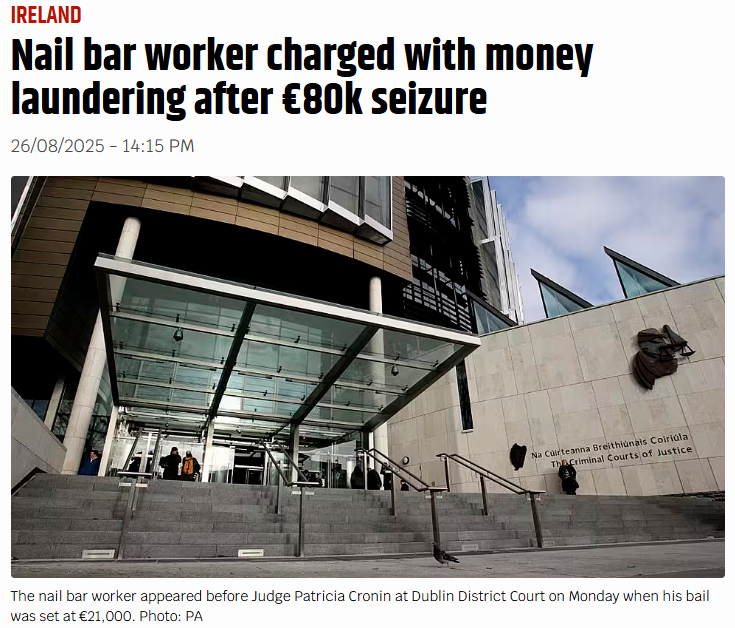

Two Guest Contributors wrote a piece on this story. See the other one here. In late August 2025, a Dublin District Court case drew renewed attention to the use of cash-intensive businesses as potential vehicles for money laundering. Gardaí seized more than €78,000 and £10,800 from the home of a nail bar worker who claimed the funds were pooled from friends to open a new salon in Drogheda. While the accused insisted the cash was legitimate, the identities of these “friends” were never verified. Charged under section 7 of Ireland’s Criminal Justice (Money Laundering and Terrorist Financing) Act 2010, the case highlights the vulnerability of cash-based enterprises, such as nail bars, hairdressers, and takeaways, to exploitation by criminals seeking to disguise illicit proceeds.

Cash-intensive businesses (CIBs) are particularly attractive to launderers because their normal operations involve large volumes of physical currency, much of it untraceable. This environment creates opportunities to blend “dirty” money with legitimate earnings. A nail bar might take in hundreds of small cash payments daily, which makes it difficult for regulators or auditors to identify whether declared revenue figures accurately reflect real customer activity. By simply overstating takings, a business can introduce illicit cash into its books with little outward indication of wrongdoing. The laundering process often begins with placement: introducing the illegal funds into circulation. In the case of a CIB, this might mean recording criminal proceeds as part of the day’s takings. From there, layering can occur through deliberate manipulation of records or structured deposits designed to avoid triggering automatic reporting thresholds. In Ireland, banks are obliged to flag cash lodgements above €10,000, but launderers often “smurf” deposits, breaking down large sums into smaller amounts to slip under the radar. Once lodged, the money appears as legitimate business income, allowing it to be integrated into the financial system without immediate suspicion. This mechanism is not new, but it remains a persistent challenge for Irish authorities, particularly as criminal groups adapt quickly. The relatively low barriers to entry for businesses like nail bars or food outlets—combined with their dependence on cash—make them ideal for money launderers who seek plausible cover for unexplained wealth. Unless authorities can demonstrate a mismatch between declared turnover and actual activity, these businesses can provide a convincing front. Ireland’s anti-money laundering framework has attempted to respond to such risks. Under the 5th EU Anti-Money Laundering Directive, factors such as high reliance on cash or ownership by non-resident individuals are considered elevated risk indicators. Designated professionals, from accountants to property agents, are expected to carry out enhanced due diligence and file suspicious transaction reports where warranted. Yet the practical challenge remains: small-scale cash-based businesses operate at the margins of scrutiny, often falling below the thresholds that attract regulatory attention. The Dublin nail bar case underscores the importance of vigilance in this area. Cash-intensive businesses are part of everyday life and, in most instances, perfectly legitimate. However, their very nature provides the camouflage that money launderers need. For Ireland, strengthening oversight, improving the detection of red flags, and fostering a culture of questioning suspicious narratives will be essential if such businesses are to be prevented from becoming conduits for illicit finance. Source: https://www.breakingnews.ie/ireland/nail-bar-worker-charged-with-money-laundering-after-e80k-seizure-1795607.html

0 Comments

What happened? Dutch online bank Bunq has been fined €2.6 million by the Dutch Central Bank (DNB) for failures in its anti-money laundering (AML) controls. The regulator cited serious shortcomings between January 2021 and May 2022, where Bunq failed to properly investigate and report potential financial crime indicators. [NB Bunq passports its credit institutions services into Ireland from the The Netherlands pursuant to the terms of the EU Directive 2013/36/EU]. DNB noted that Bunq had previously been warned and fined for similar weaknesses, yet meaningful improvements were not made. Despite this, Bunq maintains that it takes its gatekeeping responsibilities seriously, pointing to its use of advanced technology and ongoing system improvements. This fine comes against a backdrop of heightened regulatory scrutiny in the Netherlands, where major lenders including ING, ABN Amro, and Rabobank have also faced significant enforcement actions and legal challenges over AML control deficiencies. banks must know who their customers are, where the customers’ money comes from and what customers intend to do with financial products, e.g. payment accounts. - De Nederlandsche Bank 25 August 2025 What is important for MLROs to note from this case This case underlines the importance of sustained, demonstrable improvements in AML frameworks, particularly following regulatory warnings or fines. For an MLRO, the key lesson is that technology alone is insufficient without robust governance, oversight, and a culture of accountability. Regulators expect not only initial remediation but also evidence of lasting effectiveness in transaction monitoring, customer due diligence, and suspicious activity reporting. An experienced MLRO should recognize that repeated regulatory findings indicate weaknesses in escalation, board engagement, and risk ownership. Embedding AML into the bank’s strategic priorities—through continuous training, effective quality assurance, and proactive engagement with regulators—is essential. Failure to do so not only risks financial penalties but also reputational damage and possible criminal liability for the institution and senior management. Work conducted by the DNB DNB conducted an examination into the way in which Bunq complies with the Wwft. As part of the examination, DNB assessed how Bunq analyses and assesses its risks of facilitating money laundering and terrorist financing. In addition, it examined customer files and the transaction monitoring alerts associated with these files and conducted interviews with relevant officers. The high-risk files examined showed that Bunq was deficient in following up on its transaction monitoring alerts. As a result, signals of possible financial crime were not investigated in sufficient depth, if at all. Bunq was also unable to demonstrate why transactions with similar characteristics were reported to FIU-NL in one case and not in the other. As a result, there was a risk that unusual transactions were not detected, or not detected in time and that they were not reported, or not reported in time. Transaction monitoring deficiencies can cause illicit money flows to continue unchecked. Bunq failed to exercise adequate ongoing monitoring in the four files on which DNB's administrative fine is based. As a result, Bunq did not have sufficient insight into these customers and their transactions. Given the severity and extent of the deficiencies in these files, DNB considers the fine imposed both necessary and appropriate. What is the justification for the size of the fine? Between 2018 and 2023, DNB carried out several examinations into Bunq’s compliance with the Wwft. During these examinations various instances of non-compliance with the Wwft were identified, that were found to be both severe and culpable. DNB already took enforcement action on several occasions, including imposing a fine. However, this has not resulted in sustained compliance with the Wwft by Bunq. Following DNB’s examinations, Bunq has not made sufficient progress in complying with its statutory obligations under the Wwft. DNB has therefore decided to impose a punitive fine on Bunq due to the severity of the non-compliance with Section 3(2)(d) of the Wwft. DNB’s enforcement approach is primarily aimed at compliance with the law. In addition, the more severe and culpable the non-compliance, the sooner DNB will impose a fine. This is done on a case-by-case basis. Bunq's size and ability to pay have been taken into account, and the fact that Bunq completed a remedial programme to address the identified deficiencies after DNB's most recent examination has been taken into account in favour of the bank. Can Bunq appeal? Bunq lodged an objection to DNB's decision to impose a fine. The objection process is still pending. A decision becomes final if no legal remedy has been exercised against it. Any interested party may lodge an objection against the decision within six weeks of its date. The decision on the objection can be appealed in court within six weeks. Further appeal against the court ruling may be lodged with the Trade and Industry Appeals Tribunal (College van Beroep voor het bedrijfsleven – CBb). If no objection, appeal or further appeal is lodged, the decision becomes irrevocable. The table shows the current status of this decision. What is the gatekeeper role of the DNB? From the DNB's website: "Tackling money laundering is a priority for the government because it is key to effectively fighting all manner of serious crime. Concealing the origin of criminal proceeds enables perpetrators to steer clear of the investigative authorities and enjoy their ill-gotten gains undisturbed. The Anti-Money Laundering and Anti-Terrorist Financing Act (Wet ter voorkoming van witwassen en terrorismefinanciering – Wwft) aims to ensure that our financial system is not abused for money laundering and terrorist financing. Under this legislation, banks act as gatekeepers and are obliged to carry out anti-money laundering controls. This means that banks must know who their customers are, where the customers’ money comes from and what customers intend to do with financial products, e.g. payment accounts. Once customers are accepted, the bank must monitor them on an ongoing basis and report unusual transactions to the Financial Intelligence Unit (FIU-NL) so that the investigative authorities can examine suspicious transactions. Banks may use a risk-based approach to monitor their customers, meaning that high-risk customers will require more in-depth monitoring than low-risk customers." Sources:

Overall fraud offences have increased by 73% in the first six months of this year compared to the same period in 2024, according to provisional crime statistics from An Garda Síochána. The garda figures are subject to change, with official statistics published by the Central Statistics Office on a quarterly basis. The statistics show significant increases across most forms of fraud, with the biggest rise recorded in forgery or false instruments, which rose by 200% between January to the end of June 2025 compared to the same time last year. An Garda Síochána said "deception or other" rose by 178%, shopping or online auction fraud was up 166% and money laundering increased by 82%. Reports of "bogus tradesmen" had a 57% increase during this time compared to previous statistics for this period, while fraud relating to accommodation rose by 22% and so-called "account takeover fraud" rose by 18%.  However, gardaí said other forms of fraud decreased, including a drop of 88% in reports of counterfeit notes and coins. Instances of phishing, vishing and smishing reduced by 26% - such crimes are usually carried out online, via a phone call or text message. Insurance fraud also dropped by 45%, the figures showed. Information and statistics on other crimes are also reported. See source link below. Source: https://www.rte.ie/news/crime/2025/0818/1528888-garda-provisional-crime-figures/

Det Insp Cryan said this case highlights the role of professionals who help oil the wheels of criminality, known in the policing world as “professional enablers”. The Garda National Economic Crime Bureau (GNECB) is running several probes into suspected property frauds, Detective Inspector Michael Cryan told the Sunday Independent. This type of fraud came to prominence in June when a solicitor and a former millionaire were jailed for using fake deeds to register new owners of two Dublin houses. Det Insp Cryan said lawyers, accountants, investment advisers and company formation advisers, who are complicit through negligence or dishonesty, are increasingly being targeted in crime investigations. “The GNECB continues to target the professionals and professional enablers who commit so called white-collar crime for their own benefit or the benefit of others,” he said. “These can be solicitors, accountants and/or trusted local businesspeople. This is important as their actions erode public trust in the legal and business world. Property re-registration fraud can only work with the involvement of solicitors who use their trusted legal positions to help commit these frauds. “We have other investigations ongoing into property fraud as well,” added Det Insp Cryan, who said this type of fraud is a “relatively new” one, first surfacing in the last decade.  In June, Herbert Kilcline (63), a former solicitor, of Bessborough Parade, Rathmines, Dublin, and Philip Marley (53), of Ashtown, Dublin, were convicted in connection with using false deeds to change the registered ownership of the properties without the owners’ knowledge. Det Insp Cryan said this case highlights the role of professionals who help oil the wheels of criminality, known in the policing world as “professional enablers”. “A solicitor’s signature carries a lot of weight,” he said. One of those properties, Dublin Circuit Criminal Court heard, was rented in Phibsborough, with a lease income of €245,000 transferred to the US by Marley and never recovered. The other was a boarded-up Victorian house on St Mary’s Road in Dublin that had been repossessed by a financial institution. The fraud came to light when the St Mary’s Road property appeared on the Property Price Register in 2018 as sold to a company for €525,000, and the sale was challenged. The house has since been sold legitimately for €1.6m. Marley, helped by Kilcline, used false deeds to register two companies as the owners of the two properties. Kilcline, who is no longer a practising solicitor, was jailed for two-and-a-half years, and Marley was jailed for three years. While Marley was identified by the sentencing judge as the “orchestrator” of the fraud, Kilcline played a key role. Without Kilcline’s professional lawyer’s signature passing off fake conveyancing deeds as genuine, the scheme would not have worked, according to Det Insp Cryan. “That property registration fraud would not have worked without a solicitor’s involvement in it,” he said. Kilcline is not the only professional who has crossed the line between advising clients and actively helping them to break the law for criminal gain, but he is one of the few to be prosecuted for doing so. Cases that have been investigated by the GNECB include a solicitor who was probed for his continued representation of various members of a family notorious for making bogus insurance claims. He has not been prosecuted. And most solicitors who have received prison sentences in recent years were found to have stolen from client funds or from institutions, for personal gain. Michael Lynn (57) was jailed last year for five-and-a-half years for a €27m mortgage fraud which he used to fund his property investments. Fellow former solicitor Thomas Byrne (59) was convicted in 2013 of stealing €52m from six banks and defrauding 13 clients of their houses or money. Kilcline was in a different category as a classic “professional enabler” who rubbed shoulders with criminals, personally and professionally. The solicitor first came to Det Insp Cryan’s attention when he was leading the investigation into the murder of teenager Marioara Rostas. Just 18 years old, Ms Rostas was begging with her brother on Lombard Street in Dublin city centre when she went missing. Her body was later found in the Dublin mountains. Gangland criminal Alan Wilson was a suspect. Kilcline knew Wilson’s associates and was one of several people arrested in connection with possessing or withholding information. Kilcline later claimed to the Sunday World that he convinced one of Wilson’s associates to testify against him, and bring gardaí to the site where Marioara was buried. Despite Fergus O’Hanlon’s testimony, Wilson was acquitted by a jury in 2014. Kilcline later claimed that, as a result, his life was in danger from Wilson. Marley was among Kilcline’s more respectable clients. From north Dublin, he was flamboyant and, at one time, a wealthy businessman. He ran a male striptease act called Celtic Knights in the 1990s, before making €10m aged 33 from his student accommodation business, Ely Property Group. He was romantically involved with reality TV star Dana Wilkey, of The Real Housewives of Beverly Hills. His property group was liquidated in 2013, and he went bankrupt, owing €6.6m, in 2019. In the intervening years, Marley teamed up with Kilcline. Marley was promoting a US company that planned on taking over abandoned and derelict properties in Ireland, doing them up, and asserting squatters’ rights to claim ownership after 12 years. Kilcline was his legal adviser. Marley and Kilcline went from that to property registration fraud, which they engaged in between 2016 and 2018. At one point, Marley wrote to the Property Registration Authority, under a false name, pretending to be an employee of Kilcline. Sentencing Marley, the judge called him the “author” of the scheme that was motivated by personal gain. Professionals had been “duped” and ended up being investigated as a result of his actions, Judge Sinéad Ní Chúlacháin said. But she rejected Kilcline’s argument that he was guilty of “professional negligence” rather than criminality. It seemed Kilcline’s troubles came all at once. As he was being probed for the property fraud, he was convicted of social welfare fraud, falsely claiming disability and other payments worth €127,000. He was sentenced to 21 months in jail. Kilcline, who was impacted by thalidomide – the morning-sickness drug that caused birth defects in thousands of babies born worldwide in the 1950s and 1960s – blamed the fraud on his difficulty in accessing compensation. Kilcline’s lawyers told the court that he had been a “covert human intelligence source” for gardaí, his life had been threatened, and gardaí uncovered “two separate conspiracies to murder him”. A spokesperson for Tailte Éireann, a state agency responsible for property registrations, said it cannot comment on any active investigation. “We actively assist An Garda Síochána with any requests received. Tailte Éireann has a dedicated counter-fraud unit that seeks ways to combat property fraud,” the statement said. “One such initiative is Property Alert. This is a free service that provides an early notification, by email and/or text message, of certain activity on a property that you are monitoring. This allows you to take prompt action if you believe the activity is unexpected.” Source: https://www.independent.ie/irish-news/crime/gardai-home-in-on-lawyers-and-accountants-involved-in-suspected-property-fraud/a505807651.html

We have a category for "Money Mules" on the right. Given the prevalence of money mule cases in Ireland, thought this piece from the UK FCA might be of interest. Fintechs and digital banks are particularly exposed to the risk of money mules, the research found. RUSI said banking-as-a-service (BaaS) companies that provide payment or lending services to other fintechs were particularly exposed — receiving 10 per cent of payments it tracked from money mule accounts. Hard stats:

Andrea Bowe, a director at the FCA overseeing its work on fraud and financial crime, said the watchdog was working with financial firms, law enforcement and international counterparts. The regulator is also eager for tech companies to do more, given recruitment of mules often happens on social media, she said. “We recognise the scale of the challenge in tackling fraud generally, which is why fighting financial crime is one of the pillars of the new strategy announced this year by the FCA,” she said. Research released on Thursday by the Royal United Services Institute, a security think-tank, has found money mules are playing a “significant role” in enabling fraud to become “a national security threat, undermining the rule of law and threatening the financial sector”. The RUSI research, based on data from Lloyds Banking Group, urged financial services companies to share more real-time data to tackle the problem, particularly as more than half of funds received by money mules is paid out within an hour. Fintechs and digital banks are particularly exposed to the risk of money mules, the research found. RUSI said banking-as-a-service (BaaS) companies that provide payment or lending services to other fintechs were particularly exposed — receiving 10 per cent of payments it tracked from money mule accounts. “New entrants to the market, such as BaaS providers, also appear to be being exploited by fraudsters,” RUSI said. “This calls for a robust regulatory response.” The Lloyds data showed that 57 per cent of the funds flowing through money mule accounts exited via the UK’s Faster Payment system to other accounts and 20 per cent by value went to a single digital finance firm, which was unidentified. About 10 per cent of the funds were withdrawn from money mule accounts in cash via ATMs or branches, RUSI said, while nearly a fifth went on debit card payments, including some to international money transfer companies. A much smaller amount, less than 1 per cent, went to cryptocurrency exchanges. “While it has been known about for many years, there are signs that the number of money mules is growing,” said Kathryn Westmore, senior research fellow at RUSI. “It is generally like a game of whack-a-mole, where you tackle it in one area and it pops up in another.” However, despite rising concern about the issue, there has been a sharp fall in the number of money mules being reported to the UK national fraud database, which can result in the person being blocked from opening another bank account for six years.

Industry experts say the sharp drop in money mule reporting reflects calls by the authorities for financial firms to treat vulnerable customers better instead of any reduction in fraud or in the targeting of young people to launder funds. “The key driver here is very large regulated entities responding to changing guidance from a regulator — that is borne out in the significant drop in filings relating to younger people,” said Simon Miller, director of policy, strategy and communications at Cifas. The government said last year it would work with banks and local authorities to ensure “vulnerable or exploited people” were not removed from the banking system. The FCA this year urged firms to improve how they treat customers in vulnerable circumstances. Miller said the drop in filings could also partly reflect a change in Cifas reporting rules to avoid banks filing cases where they only suspect someone of being a money mule rather than having evidence they were complicit — but this was thought to have only had a marginal effect. He added that more money mules were being trained by their recruiters in what to tell banks when they are questioned, which may have contributed to the lower number of filings. More people are handing over their identities to allow fraudsters to open separate accounts in their name. Ben Donaldson, managing director for economic crime at trade body UK Finance, said many money mules were tricked or coerced into it without knowing it is a crime for which they could be imprisoned, even though few are convicted. “I don’t think we can say all mules are victims but certainly many mules are victims, so it’s a complicated problem,” he said. Source: https://www.ft.com/content/6f517e05-0561-442f-842f-72eba8d125f3

Assistant Commissioner Paul Cleary, from the Dublin Metropolitan Region, said: “This significant seizure of cash not only removes ill-gotten gains from the hands of criminals, but also deprives them of money they would have used to fund further criminal activities and cause harm in our communities.”

The discovery was made as part of an operation targeting an organised crime gang involved in the sale and supply of controlled drugs and money laundering activities in the Dublin area Three men have been arrested in Dublin after gardaí found almost €350,000 in cash stuffed inside a suitcase in a car. The discovery was made as part of an operation targeting an organised crime gang involved in the sale and supply of controlled drugs and money laundering activities in the Dublin area. The car was searched in Drumcondra on Friday. The operation was carried out by the Dublin Crime Response Team (DCRT) who searched three men, who were passengers in the vehicle, and their luggage, and located and seized an estimated €345,640 cash. Three men, aged in their 40s, were arrested by gardaí and are currently being detained at garda stations in the Dublin region. Assistant Commissioner Paul Cleary, from the Dublin Metropolitan Region, said: “This significant seizure of cash not only removes ill-gotten gains from the hands of criminals, but also deprives them of money they would have used to fund further criminal activities and cause harm in our communities.” Source: https://www.irishexaminer.com/news/courtandcrime/arid-41676992.html

Paul Chowles, 42, stole the proceeds of an online illegal drugs market and laundered the money on the dark web

Definitely a great AML typology for MLROs' training kit and of course a useful Know Your Employee one as well. I would love to hear from current law enforcement officers and the many ex law enforcement officers in the network on their thoughts on this case. A National Crime Agency (NCA) officer has been jailed for stealing £4.4m worth of bitcoin seized during a joint operation with the US Federal Bureau of Investigation (FBI), after the criminal he was investigating told the police it was missing. Paul Chowles thought he had got away with the crime for five years, prosecutors said, after laundering the money on the dark web and spending £613,000, mostly on day-to-day expenses. The 42-year-old had been working as an investigator on the case of Thomas White from Liverpool, who ran an online black market for illegal drugs, known as Silk Road 2.0, launched a month after a website of the same name was shut down in 2013 by the FBI. It was White, while under investigation, who noticed someone had taken 50 bitcoin of the 97 he had, and told police it had to be someone inside the NCA because they had the private keys for his cryptocurrency wallet. Merseyside police, which had responsibility for managing White in the local area following his release on licence in early 2022, discussed the theft with the NCA, in meetings that Chowles attended. During the investigation, officers discovered Chowles had stolen the money between 6 and 7 May 2017, two years after the White investigation was over, and in the following five years had been spending it in supermarkets and hardware stores and on fuel and meals, with investigators uncovering hundreds of debit card transactions. What are some of the lessons from this case? Generally, the case of the NCA officer jailed for stealing seized bitcoin offers sobering lessons for Money Laundering Reporting Officers (MLROs) and law enforcement agencies. It underscores the critical threat posed by insider abuse and the importance of knowing your employees—especially those entrusted with sensitive financial or digital assets. More specifically, here are 5 Key Lessons for MLROs and Law Enforcement. Key Lessons for MLROs and Law Enforcement 1. Insider Threats Are Real and Costly Even trusted officers can exploit access for personal gain. Chowles used his position to divert seized Bitcoin, bypassing internal controls. Insider threats are harder to detect than external ones because they exploit legitimate access. 2. Know Your Employee (KYE) Is as Crucial as KYC Background checks, ongoing vetting, and behavioral monitoring are essential. Chowles had no prior criminal record, but his misuse of crypto tools went unnoticed for years. Agencies must implement continuous risk assessments for staff in sensitive roles. 3. Weak Internal Controls Enable Exploitation Chowles used mixing services to obscure transactions—a red flag for MLROs. Lack of multi-signature wallets, audit trails, and real-time monitoring allowed the theft to go undetected. Agencies must adopt blockchain analytics tools and segregation of duties. 4. Training in Crypto Forensics Is Vital Law enforcement and MLROs must understand crypto mechanics, including wallets, mixers, and blockchain tracing. Chowles exploited gaps in institutional knowledge to cover his tracks. Regular training and collaboration with tech experts can close these gaps. 5. Reputation and Public Trust Are at Stake This case damages the credibility of the NCA and raises doubts about asset integrity. MLROs must ensure that seized assets are handled transparently and securely. Agencies should publish audit results and enforce accountability to rebuild trust. What are some of the strategic takeaways from this case?  Sources:

A very interesting case study / typology for fast growing digital banks, payments firms and crypto-asset services providers and indeed any fintech in any country where there are anti-money laundering requirements.

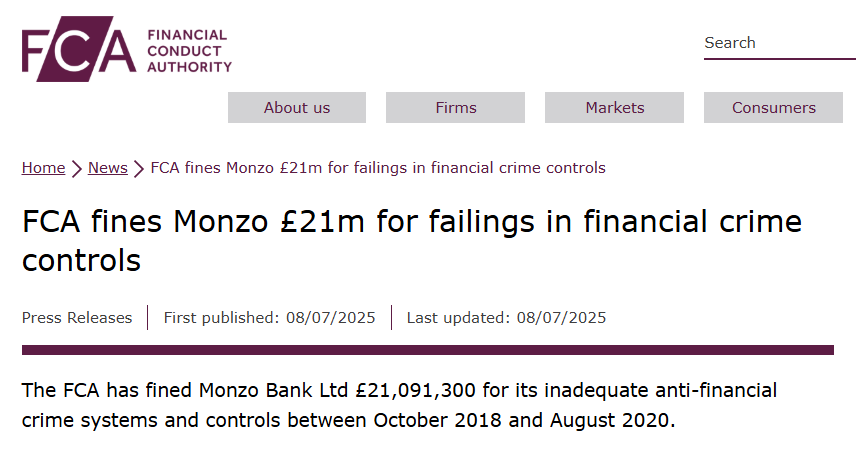

A few days ago our Peter Oakes wrote a piece on Linkedin about Monzo Bank's continuing plans to establish an authorised bank in Ireland. See https://www.linkedin.com/feed/update/urn:li:activity:7347556992883843072. Today the UK Financial Conduct Authority issued an enforcement notice and fine of £21mn against the rapidly growing digital bank. Hope this short blog helps financial crime professionals and MLROs with some useful thought for AFC training and the typology library. 📈 As Growth Accelerates, So Must Your Controls Rapid client onboarding and frequent product rollouts increase exposure to money laundering (ML) and terrorist financing (TF) risk. Firms often focus on scaling—the tech stack, user experience, marketing—while compliance lags. Regulatory expectations, however, demand that internal controls scale simultaneously. Digital banks must avoid the “too little, too late” trap. A detailed, documented risk assessment underpins everything: products, client segments, geographies, channels. That assessment must inform transaction monitoring rules, reporting thresholds, enhanced due diligence, ongoing review, staff training, management information (MI), and audit cycles. 🛡️ Foundation: AML/CTF Risk Assessment * Per Irish and EU standards, and echoed in Central Bank of Ireland guidance, your AML/CFT framework must include key elements: * Thorough risk assessment at the outset and with any material change (new product, geography, channel) * Board and senior management oversight with regular MI and challenge sessions * Tailored governance, controls, training, and testing based on risk This creates the durable infrastructure needed for AML resilience. 🧱 Case Study: Monzo’s £21M Fine for AML Failings In June 2025, the FCA levied a £21 million penalty on Monzo, citing systemic weaknesses in financial crime control frameworks as the firm scaled its product footprint. The FCA’s Final Notice (link below) highlighted:

👉 Access the case materials from FCA: “FCA fines Monzo £21 m for failings in financial crime controls”

This is a red flag for high-growth fintechs: internal control gaps are not just theoretical—they trigger high-profile enforcement. 🧭 Key Tactical Takeaways

✍️ Final Word for MLROs As MLROs at high-growth firms, your role is to translate risk into action. Ensure your AML/CFT framework is not just documented—but truly operational across all products and regions. Be proactive, visible, and predictive.

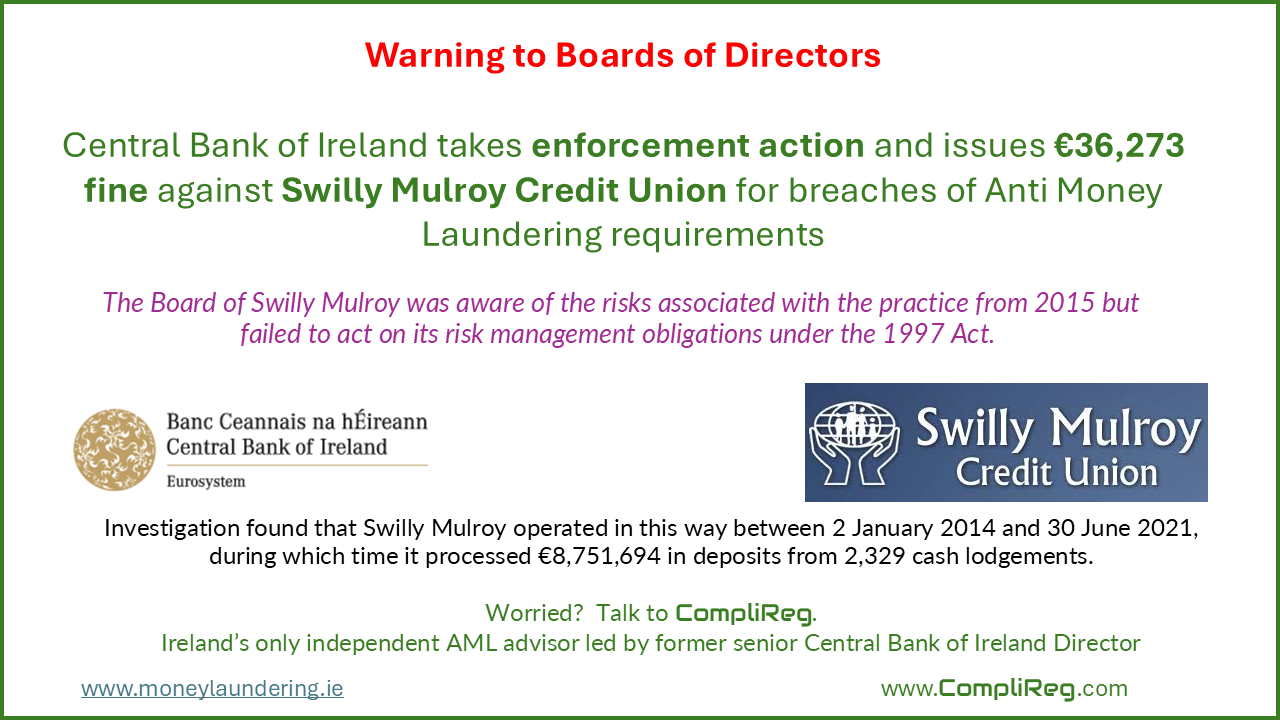

The Board of Swilly Mulroy was aware of the risks associated with the practice from 2015 but failed to act on its risk management obligations under the 1997 Act. CENTRAL BANK OF IRELAND PRESS RELEASE – Wednesday 2 July 2025 The Central Bank takes enforcement action against Swilly Mulroy Credit Union for breaches of Anti Money Laundering requirements. The Central Bank of Ireland (the Central Bank) has fined Swilly Mulroy Credit Union (Swilly Mulroy) €36,273 for breaching requirements of the Criminal Justice (Money Laundering and Terrorist Financing) Act 2010 (the 2010 Act) and the Credit Union Act 1997 (the 1997 Act). The 2010 Act requires firms to put in place safeguards against the risk of money laundering and the 1997 Act requires credit unions to develop and implement risk management systems to monitor and manage risks. The Central Bank’s investigation found that Swilly Mulroy operated a practice of soliciting and accepting cash from depositors who did not hold accounts with the Credit Union. This money would then be electronically transferred to a branch of a local bank, without first being deposited in an account in the customer’s name at Swilly Mulroy. As a result, Swilly Mulroy failed to conduct the necessary Anti-Money Laundering checks on the depositors and the transactions. This specific cash intensive practice had been flagged to the credit union sector as presenting a heightened money laundering risk. Investigation found that Swilly Mulroy operated in this way between 2 January 2014 and 30 June 2021, during which time it processed €8,751,694 in deposits from 2,329 cash lodgements. The investigation found that Swilly Mulroy operated in this way between 2 January 2014 and 30 June 2021, during which time it processed €8,751,694 in deposits from 2,329 cash lodgements. The Board of Swilly Mulroy was aware of the risks associated with the practice from 2015 but failed to act on its risk management obligations under the 1997 Act. A new management team ceased the practice in 2021 and subsequently brought it to the attention of the Board.

The issue was not brought to the Central Bank’s attention and was discovered in 2022 during an inspection by the Central Bank’s Anti-Money Laundering Division. The Central Bank commenced this enforcement investigation in 2023. The investigation yielded multiple examples of cash lodgements, which in the usual course should have triggered additional and careful scrutiny but instead were processed without any Anti-Money Laundering checks. Swilly Mulroy has therefore breached multiple requirements of the 2010 Act. Swilly Mulroy has admitted the prescribed contraventions and has agreed to the undisputed facts as set out in the attached Settlement Notice. As part of the settlement agreement reached between the Central Bank and Swilly Mulroy, the Central Bank has determined that sanctions comprising a reprimand and monetary penalty in the amount of €51,819 are both warranted and proportionate to the size of the firm. The application of a 30% settlement scheme brings the amount to €36,273. The sanctions have been accepted by Swilly Mulroy. The sanctions are subject to confirmation by the High Court and will not take effect unless confirmed. Colm Kincaid, the Central Bank’s Director of Enforcement, said: “Anti-money laundering and counter terrorist financing legislation is designed to prevent the financial system being used to launder the proceeds of crime or fund terrorist activities. One of its key safeguards is that regulated financial service providers have controls in place to identify their customers and detect potential money laundering or terrorist financing. Where firms allow gaps in their control framework, they create opportunities for criminals and terrorists to use our financial system to pursue their illegal activities. It is also important that, when firms identify that such control gaps exist, they must report it to the Central Bank, so that appropriate actions can be taken to manage and mitigate the risk. This action demonstrates the Central Bank’s continued focus on firms’ compliance with their legal obligations to safeguard the integrity of our financial system.”

The money laundering trial of former Ireland hockey international Caitriona Carey is expected to last four to six weeks and will go ahead in January 2027 before Dublin Circuit Criminal Court.

The 47-year-old, with an address at Rochford Manor, Graiguecullen, Co Carlow, is charged with three offences contrary to Section 7 of the Criminal Justice (Money Laundering and Terrorist Financing) Act 2010, one over a 12-month period in 2019, one in 2020 and one in 2021. Source: https://www.breakingnews.ie/ireland/money-laundering-trial-of-former-hockey-star-caitriona-carey-set-for-2027-1778715.html |

AuthorOn this page you will find a selection of links to articles useful for AFC training. Archives

June 2026

Categories

All

|

RSS Feed

RSS Feed